The supply & demand economics behind the current VC boom and crunch

Print

20 February 2016

Adley Bowden / PitchBook Blog

Overnight it seems the venture industry has ground to a standstill. The ‘unicorn’ term now means overly inflated valuation in the process of negotiating a down round. The daily news is now full of departing CEOs, layoffs, zombie unicorns and who’s next punditry. How did this all happen and with such speed? Is there an economic model that can explain the boom and bust of this complex market?

Well, it turns out its pretty simple—a shift in the demand curve for venture capital followed by two shifts in the supply of venture capital led to a market way out of its long run equilibrium range. This led to a fragile situation where the recent market correction caused a dramatic short-term shift in supply of venture capital, taking us to where we are now.

Supply & Demand of Venture Capital

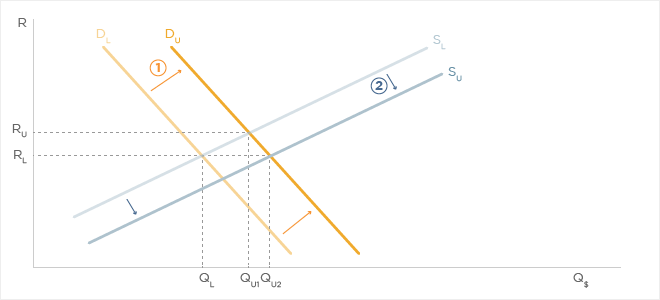

In the venture market, Demand for venture capital is essentially the number of companies looking for venture funding. The Supply is the amount of venture capital investors are willing to invest in companies given a rate of return (inverse of price at which they will invest). The supply is fairly elastic (capital flows easily in today's environment) and the demand inelastic (due to power law of venture outcomes), leading to a chart that looks like the one below. For more reading, see: What Drives Venture Capital Fundraising by Gompers & Learner.

The Unicorn Era Demand Shift

At some point around 2012 it seems that a shift in the Demand for venture capital occurred. This pushed up the demand curve line to Du, creating a larger number of higher performing companies/investments, resulting in the corresponding movement along the supply curve to a higher level of funding (Qu). There are several drivers of this shift, including smartphone proliferation, software eating the world and biotech boom, among others, that led to the sudden increase in innovation and disruption opportunities over the last couple of years.

With this shift the long run rate of return expectation for venture (Rl) was below the new unicorn era returns (Ru). This led to a shift in the supply of venture capital as limited partners and venture firms identified the beginning of another venture boom and rushed to supply more capital to meet this demand. The result is our unicorn era supply shift (Su).

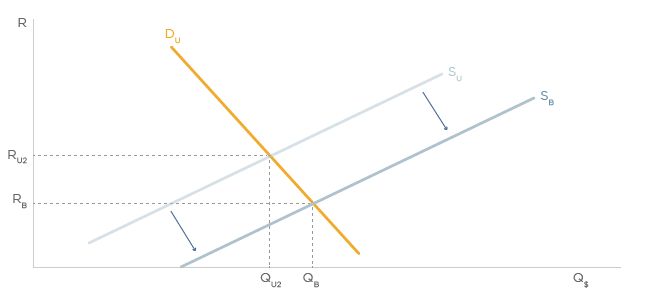

The Bernanke/Yellen Supply Shift

We have a joke at PitchBook that we should thank Bernanke for Uber. What we mean by that is that as a result of the zero interest rate environment, a large group of investors (mutual funds, hedge funds, private equity, multinational corporations, etc.) starved for returns plowed money into the unicorn era extremely attractive venture market. Looking at the data, this begins to have a significant impact starting in 2014. It was this movement of non-traditional investors (aka venture tourists) into the venture market that caused what we call the Bernanke supply shift (SB).

This pushed the equilibrium return rate way below the long run rate and dramatically increased the quantity of capital invested from Qlto QB. Worth noting the RB was perceived at the time to still be a good return considering other asset returns at the time. Looking at the actual data, this is seen in the increase from $44 billion in U.S. venture investments in 2013 to $77 billion in 2015. The result of all the new capital flowing into venture was that a lot of companies that wouldn’t traditionally have made the investment cut did, and were able to raise more capital at higher valuations than ever before. This will likely show in the data over the next few years but anecdotally it has been an undercurrent from VC ‘old-timers’ for the last 18 months or so.

PANIC… errr 2016 Supply Shock

This takes us up to basically last fall. In September the market wobbled, public tech took a bit of a hit and everyone grabbed the table like you do when you think you might have just felt an earthquake. This primed the venture market and had people on edge, so when the public markets correction hit tech and biotech over the last few weeks investors slammed on the brakes. This is known as a supply shock in economics and though it has been only a matter of days since this started, we are looking at this currently as a short-term supply shock.

The effects of a supply shock are that our supply of capital suddenly moves very far left (SS16) as investors suddenly and dramatically raise the return rate threshold (RS16) for making a new investment. Basically we enter into an environment where only the best of the best get funded. Everyone else gets coached on burn rates, unit economics and what a ratchet means.

So what does the future hold?

With the multiple supply and demand shifts, the venture market retrospectively clearly moved to a fragile spot where at the first sign of a wobble everyone was headed for the exit doors. However, if you look back at the root drivers of the shifts they likely still exist (rapid innovation, new technologies, low interest rates, etc.). Did investors maybe misperceive the demand shift and think it had moved further than it did? Probably. Did non-traditional investors think their venture investments were going to generate a higher rate of return with less risk then they will? Probably.

We expect over the short term for the supply curve to stay left and the demand curve to also likely shift down. Looking further out (12 to 18 months), we still believe a lot of positive tailwinds will exist and that a new level of investment will get set beyond the previous long-term equilibrium closer to our unicorn era equilibrium as the aforementioned forces support more demand and supply of venture investment.

So there you have it according to a macro economic supply and demand model—it's simply a short-term supply shock following a shift in demand and two shifts in supply.

All Portfolio

MEDIA CENTER

-

The RMI group has completed sertain projects

The RMI Group has exited from the capital of portfolio companies:

Marinus Pharmaceuticals, Inc.,

Syndax Pharmaceuticals, Inc.,

Atea Pharmaceuticals, Inc.