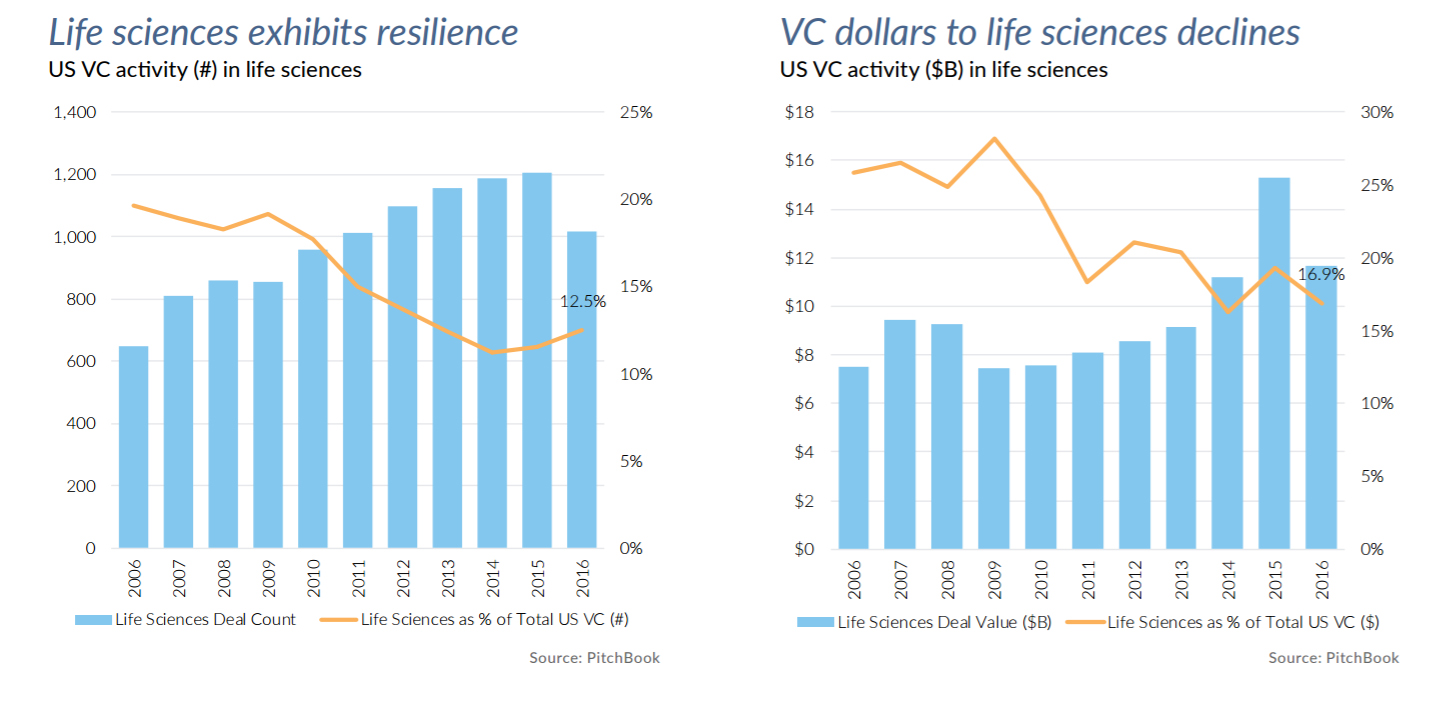

Venture Monitor: 2016 ended with a total of $69.1 billion invested into the US venture ecosystem, representing the second highest annual total—after 2015—in the past 11 years

Print

12 January 2017

PitchBook

Through the first half of 2016, venture investment activity in the US seemingly continued the frenetic pace of 2015, which was a headline year for the industry. However, a slowdown in VC investment activity began in the third quarter that continued into the fourth quarter when just $12.7 billion was deployed to 1,736 companies. Nonetheless, 2016 ended with a total of $69.1 billion invested into the US venture ecosystem, representing the second highest annual total—after 2015—in the past 11 years. More than 7,751 companies raised capital across 8,136 deals in 2016, with both measures reverting toward 2012 annual levels.

Through the first half of 2016, venture investment activity in the US seemingly continued the frenetic pace of 2015, which was a headline year for the industry. However, a slowdown in VC investment activity began in the third quarter that continued into the fourth quarter when just $12.7 billion was deployed to 1,736 companies. Nonetheless, 2016 ended with a total of $69.1 billion invested into the US venture ecosystem, representing the second highest annual total—after 2015—in the past 11 years. More than 7,751 companies raised capital across 8,136 deals in 2016, with both measures reverting toward 2012 annual levels.

Driven by an updraft in valuations, the number of deals during this period escalated, creating indigestion in the marketplace for some. As a result, 2016 represented less of a slowdown and more of a return to normalization. Venture investors are now circling back to tried and true ways of deploying capital and being much more critical of their investment options. Going into 2017, the question remains whether venture investment activity has plateaued, or if it will continue to downshift.

It was against this backdrop of a return to normalcy that the venture industry notched its best fundraising year of the past decade in 2016.

Each quarter of 2016 saw strong fundraising totals, with the $13.6 billion raised during the second quarter being the standout. In the fourth quarter, venture investors raised $7.3 billion across 50 funds, bringing the annual total to $41.6 billion raised across 253 funds.

Despite the 10-year high for capital raised by venture funds, the total number of funds closed in 2016 declined slightly for the second

straight year. The cyclical nature of venture capital fundraising, evidenced by a number of larger venture firms coming back to market and closing $1 billion+ funds, coincided with more capital being managed by fewer funds, leading to an increasing concentration of capital in the industry. Seven firms raised $1 billion+ venture funds in 2016, accounting for more than 23% of the total capital raised. Given how strong fundraising was in 2016, it will be telling to see how the fundraising environment shakes out in 2017, especially for smaller funds and new managers who may encounter a challenging climate.

In the face of a strong year for fundraising, the exit environment remained a challenge. Corporate acquisitions continued to account for the largest proportion of venture-backed liquidity events in 2016, and the IPO window remained narrow for venture-backed companies.

In the fourth quarter, seven venture-backed companies went public, bringing the total for the year to 39, which is half the number of IPOs from 2015 and the lowest completed since 2009, when there were only 10 venture-backed IPOs in the wake of the financial crisis.

Looking to 2017, there is widespread hope that the IPO market will finally thaw. With around 20 venture-backed companies currently

in IPO registration, there is optimism for a strong 2017. Though the quantity and quality of companies in the pipeline remains high, the execution of those IPOs may pose a challenge, especially for companies that have valuations that might not be easily supported in the public markets. While there is optimism for a strong year of IPO activity, M&A activity will likely remain robust with plenty of cash on corporate balance sheets and expectations of a Republican-controlled Washington fulfilling its pledge to reform the corporate tax code.

In spite of the slowdown in venture investment activity in the second half of 2016 and questions surrounding the IPO environment for venture-backed companies, there remains much to be optimistic about in 2017. Venture investors will continue to invest in and unlock new innovations that will transform our society and strengthen our economy. Many venture investors forecast 2017 being categorized as “the rise of the machine” with an increased emphasis on investment in artificial intelligence, robotics, drones and machine learning. In fact, many investors will increasingly experiment in “exploratory sectors” to determine what trends they can learn from, as they realize that to make interesting, disruptive investments, they need to look beyond what they are already doing.

Full report here

All Portfolio

MEDIA CENTER

-

The RMI group has completed sertain projects

The RMI Group has exited from the capital of portfolio companies:

Marinus Pharmaceuticals, Inc.,

Syndax Pharmaceuticals, Inc.,

Atea Pharmaceuticals, Inc.