The top 15 spenders in the global drug R&D business: 2017

Print

25 April 2017

John Carroll / Endpoints News

You usually don’t see much annual fluctuation in the overall R&D budgets of the top 15 companies. The trend over the last few years has been to keep the lid on spending, particularly among the giants in Big Pharma. Companies didn’t cut much overall, but there was plenty of realignment going on as the industry refocused pipelines and continued a migration to the big hubs.

This past year, though, it was clear that a few companies wanted to turn up the heat in drug development, and this kind of fuel costs real money for companies that traditionally focus heavily on late-stage blockbuster drug research.

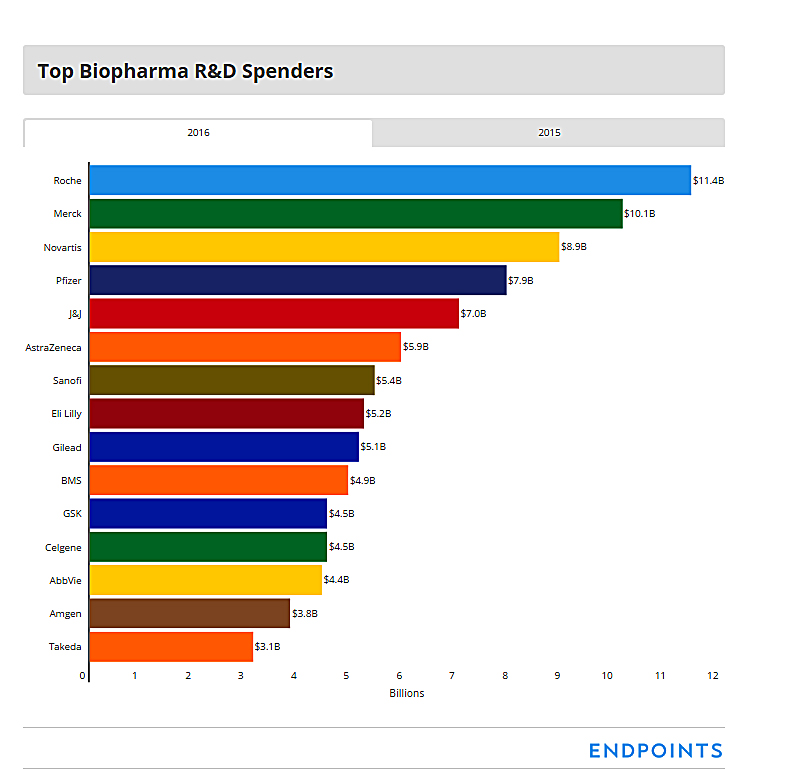

The top five in the business saw their collective spending jump by more than $5 billion, from 2015 to 2016, based on the annual numbers filed largely — though not entirely — with the SEC and gathered by Endpoints News. Two of those companies, Roche and the new number 2, a hard charging Merck, accounted for the lion’s share of the increase. (To be sure, some onetime non-R&D spending, such as Merck’s patent settlement with Bristol-Myers on Keytruda, figured in. But so did bread and butter spending.)

Gilead also saw a significant increase in research costs, with Eli Lilly — now off course following two bad setbacks for solanezumab and baricitinib — and the ever aggressive Celgene joining the action as they pressed the accelerator on new drug programs.

Curiously, the added spending coincided with a bad drop in new drug approvals in 2016. But they don’t correlate, and we’ve already seen that turnaround under way as regulators get busy with a brand new year — and soon a brand new FDA commissioner.

Paradoxically, one of the reasons why some of these R&D budgets have been rising is that development has been picking up speed. That’s abundantly clear now in the cancer field, where success with immuno-oncology has triggered a land rush mentality, with top players staking out as much territory as fast as possible. Anything left on the table won’t stay there for long, and first mover advantage can be critical. So invest now, reap your rewards later.

In the process, treating new oncology cases is gradually being revolutionized. And that’s not PR talk.

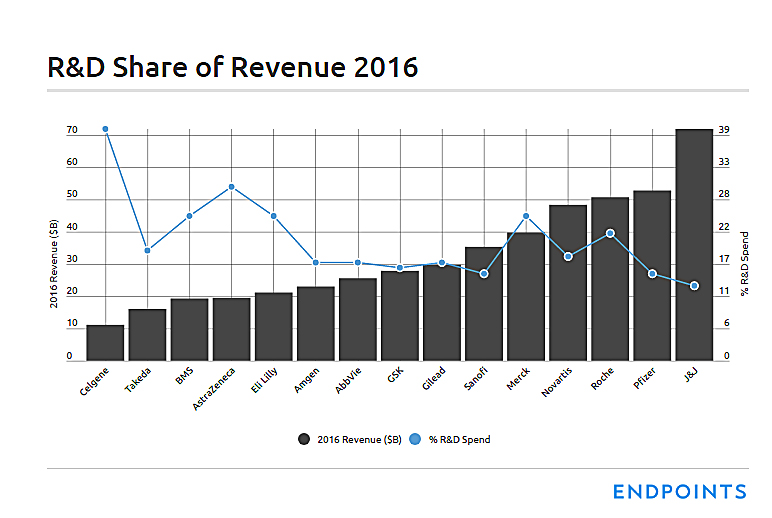

R&D reorganization, once aimed at massive cost cutting several years ago at places like Merck, GlaxoSmithKline, Pfizer and AstraZeneca, is still with us. But the form and substance has changed. Now these companies, along with a pressured Novartis and a bottom-line focused Amgen, have been looking to winkle out cost savings wherever they can be found. But many are also investing heavily in new R&D centers in San Francisco and Boston/Cambridge.

Meanwhile, some of the top players, like Sanofi, increasingly appear to be stuck. Their in-house organizations have been largely unproductive. Their partnerships are responsible for turning out the key new approvals.

We’ve seen some M&A deals, of course, but not an abundance of acquisitions from the big 10. Roche doesn’t feel it needs to. Merck hasn’t been buying much. AstraZeneca — which is increasingly cash restricted — has been selling off its disappointments, ginning some cash flow in the process.

The M&A standouts have been Pfizer (of course) and J&J, which carefully stepped up to buy Actelion’s portfolio for $30 billion. AbbVie is getting a rep for overspending on its deals.

Meanwhile Sanofi practically has to do a deal to prove it knows how after letting Medivation and Actelion slip through its fingers, and not just to higher bids. And Gilead is being ordered to get into gear by analysts who have been kept waiting too long.

We’re still waiting for the big one.

And that remains the key here. Perhaps after tax reform, if that happens, we’ll see some of those overseas billions put to use in buyouts. But it’s a long time coming.

All Portfolio

MEDIA CENTER

-

The RMI group has completed sertain projects

The RMI Group has exited from the capital of portfolio companies:

Marinus Pharmaceuticals, Inc.,

Syndax Pharmaceuticals, Inc.,

Atea Pharmaceuticals, Inc.